01 May

Transfer Pricing under UAE Corporate Tax

Understanding UAE Transfer Pricing Rules under Corporate Tax Law

With the introduction of UAE Corporate Tax, Transfer Pricing (“TP”) has become one of the most important compliance areas for businesses operating in the UAE. Companies dealing with related parties, group entities, shareholders, or cross-border transactions are now required to ensure that such dealings comply with the Arm’s Length Principle under UAE Corporate Tax law.

The UAE has aligned its Transfer Pricing framework with internationally accepted OECD Transfer Pricing Guidelines, bringing the country in line with global tax standards and increasing transparency in related party transactions.

This article explains the fundamentals of Transfer Pricing in the UAE, its applicability, documentation requirements, and practical compliance considerations for businesses.

What is Transfer Pricing?

Transfer Pricing refers to the pricing of transactions between related parties or connected persons. These transactions must be carried out at prices that independent parties would agree upon under similar circumstances.

In simple terms, UAE businesses cannot artificially increase or reduce prices in related party transactions to reduce taxable profits.

Examples of related party transactions include:

- Management fees

- Consultancy charges

- Intercompany loans

- Royalty payments

- Shared services

- Purchase or sale of goods

- Director/shareholder transactions

- Cost allocations between group companies

UAE Transfer Pricing Law and Regulations

Transfer Pricing in the UAE is mainly governed by:

- Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses

- Ministerial Decision No. 97 of 2023

- OECD Transfer Pricing Guidelines

The UAE Corporate Tax regime adopts the internationally recognized Arm’s Length Principle, requiring related party transactions to reflect fair market value.

Who is Required to Comply with Transfer Pricing Rules in UAE?

Transfer Pricing provisions apply to:

Mainland Companies

All taxable mainland UAE businesses with related party transactions.

Free Zone Companies

Free Zone entities, including those claiming 0% Corporate Tax benefits, must also comply with Transfer Pricing regulations.

Group Companies

Businesses operating under common ownership or management.

Shareholders and Connected Persons

Payments made to shareholders, directors, owners, or connected persons must be commercially reasonable.

Cross-Border Transactions

International transactions between UAE and foreign group entities are also covered.

Understanding Related Parties and Connected Persons

Under UAE Corporate Tax law, related parties may include:

- Parent and subsidiary companies

- Sister concerns

- Companies under common control

- Relatives and family-owned businesses

- Shareholders and directors

Connected persons generally include:

- Owners

- Directors

- Partners

- Their relatives or controlled entities

Transactions with connected persons may attract scrutiny if they are not properly supported or commercially justifiable.

Arm’s Length Principle in UAE Transfer Pricing

The Arm’s Length Principle is the foundation of UAE Transfer Pricing rules.

This means:

Transactions between related parties should be priced in the same manner as transactions between independent third parties.

For example:

- Intercompany loans should carry reasonable interest rates.

- Management fees must be supported by actual services rendered.

- Shared expenses should be allocated fairly and logically.

The Federal Tax Authority (FTA) may challenge arrangements that appear artificial or tax-driven.

Transfer Pricing Documentation Requirements in UAE

Businesses may be required to maintain proper Transfer Pricing documentation.

-

Transfer Pricing Disclosure Form

Certain businesses must submit a disclosure form along with their Corporate Tax Return.

The form generally includes:

- Related party transactions

- Connected person transactions

- Nature and value of dealings

-

Master File and Local File

Businesses meeting prescribed thresholds may also need to maintain:

Master File

Contains:

- Group structure

- Business overview

- Global TP policies

Local File

Contains:

- UAE entity transactions

- Pricing methodology

- Benchmarking analysis

- Financial information

Common Transfer Pricing Risk Areas in UAE

Intercompany Service Charges

Management and consultancy fees without supporting documentation may be disallowed.

Interest-Free Loans

Related party financing without commercial interest terms may attract adjustments.

Free Zone and Mainland Transactions

Special attention is required where Free Zone entities transact with mainland companies.

Excessive Director or Shareholder Payments

Compensation lacking commercial justification may not be deductible.

Cross-Border Transactions

Foreign withholding tax exposure and Permanent Establishment (PE) risks should also be evaluated.

Practical Transfer Pricing Compliance Tips

Businesses should proactively:

✅ Identify all related party transactions

✅ Maintain written intercompany agreements

✅ Document pricing methodology

✅ Benchmark material transactions

✅ Keep supporting invoices and records

✅ Review shareholder/director transactions annually

✅ Assess cross-border tax implications before entering transactions

Why Transfer Pricing Matters in UAE

Transfer Pricing impacts several areas of Corporate Tax compliance, including:

- Deductibility of expenses

- Taxable profits

- Group structuring

- International taxation

- Audit risk

- FTA compliance

As the UAE Corporate Tax regime matures, Transfer Pricing is expected to become a key focus area for tax audits and regulatory reviews.

Conclusion

The introduction of Transfer Pricing under UAE Corporate Tax marks a significant shift in the UAE’s tax environment. Businesses with related party transactions must now ensure that pricing arrangements are commercially justifiable, properly documented, and compliant with the Arm’s Length Principle.

Early planning and robust documentation can help businesses reduce tax risks, strengthen compliance, and avoid future disputes with the Federal Tax Authority.

Integrity Global Consulting

UAE • India • UK

Your Partner in UAE Corporate Tax & International Tax Advisory

For professional assistance with:

- Transfer Pricing compliance

- Related party transaction review

- Corporate Tax advisory

- TP documentation

- International taxation matters

📩 Contact our team today.

07 Jul

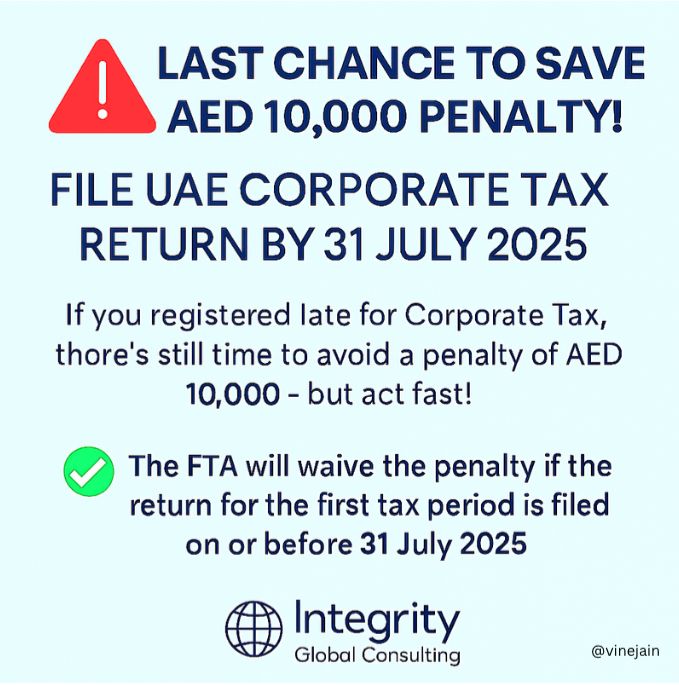

Penalty Waiver Opportunity: File UAE Corporate Tax Return by 31 July 2025

🛡️ Last Chance to Avoid AED 10,000 Penalty for Late Corporate Tax Registration in UAE

Published by Integrity Global Consulting

📅 07 July 2025

The UAE Federal Tax Authority (FTA) has announced a significant relief opportunity for businesses that missed the deadline to register for Corporate Tax.

If your company has received a penalty of AED 10,000 for late registration, there’s still a way to avoid paying it — but the window is closing soon.

✅ Automatic Waiver of Late Registration Penalty

Under the FTA’s administrative relief mechanism, the AED 10,000 penalty will be automatically waived provided the following condition is met:

✔️ The company files its first Corporate Tax Return or Small Business Relief declaration by 31 July 2025,

For tax periods ending 31 December 2024.

This relief applies even if registration was completed late — as long as the return is filed on time within the 7-month window from the period-end.

📌 Example

- First Tax Period End Date: 31 December 2024

- Tax Return Filing Deadline for Waiver: 31 July 2025

- Usual Tax Return Due Date: 30 September 2025

- ✅ Waiver applies if the return is filed by 31 July 2025

⚠️ What If You Delay Beyond 31 July?

If the return is filed after 31 July 2025 (but before the standard 30 September 2025 deadline), the penalty becomes payable and cannot be waived, even if registration and return are both completed.

💼 What Should Businesses Do Now?

- Check if your company was registered late for Corporate Tax.

- Ensure your books of accounts and financials are ready.

- File your tax return or declaration before 31 July 2025.

🧾 Need Assistance?

At Integrity Global Consulting, we are assisting UAE mainland and Free Zone entities with:

✅ Corporate Tax registration

✅ Preparation of unaudited financials

✅ Return filing through the EmaraTax portal

✅ Small Business Relief eligibility assessment

📩 Contact us today to ensure timely compliance and avoid unnecessary penalties.

#UAECorporateTax #TaxRelief #FTAUAE #CorporateTaxUAE #SmallBusinessRelief #TaxFiling #UAECompliance #IntegrityGlobalConsulting

01 May

UAE Corporate Tax – mandate to submit audited financial statements

The UAE Ministry of Finance has issued Ministerial Decision No. 84 of 2025, dated 22 April 2025, providing greater clarity on who is required to prepare and submit audited financial statements under the UAE Corporate Tax regime.

This decision is an important update for businesses operating in the UAE, especially in light of the implementation of Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses.

Key Highlights of Ministerial Decision No. 84 of 2025

Under the Ministerial Decision, the following categories of Taxable Persons are mandated to prepare and maintain audited financial statements for Corporate Tax purposes:

- Taxable Persons with Revenue exceeding AED 50 million during the relevant Tax Period.

- Qualifying Free Zone Persons, irrespective of their revenue level.

This means that businesses falling within either of the two categories must ensure their financial statements are audited by a licensed auditor in accordance with applicable accounting and auditing standards.

Effective Date

This requirement applies to Tax Periods starting on or after 1 June 2023. Hence, businesses must review their financial reporting obligations for the current and upcoming tax periods to ensure compliance.

Why Is This Important?

- Audited financial statements enhance transparency and reliability of tax filings.

- Non-compliance could potentially lead to penalties or rejection of tax positions, especially for Free Zone entities seeking to retain their 0% Corporate Tax rate as a Qualifying Free Zone Person.

- The requirement is also aligned with broader efforts to improve financial governance and regulatory compliance in the UAE.

Our Assistance

We assist companies in the UAE with:

- Preparation and audit of financial statements,

- Determination of applicability of the audit requirement,

- Corporate Tax registration and compliance,

- Advisory for Free Zone and mainland companies.

If your business falls under either of the categories mentioned above or you are unsure of your obligations, feel free to contact our team for guidance and support.

29 Jun

UAE approves guidelines for public-private partnerships

Infrastructure, energy, health, social services, education sectors first phase of focus

Abu Dhabi: The UAE approved a manual on Public-Private Partnerships (PPP), outlining a policy and procedural framework to enable federal government entities to implement projects, and benefit from the expertise of the private sector.

The UAE Ministry of Finance announced the UAE Cabinet’s approval of the manual, which supports national efforts to stimulate investment in joint projects between federal entities and the private sector. It added that the manual encourages the participation of the private sector in creating developmental projects.

“The manual governs the operations and processes for designing, planning, and implementing projects, as well as provides a summary guideline for federal entities and private sector partners to follow in partnership projects, ensuring transparency and clarity for all concerned parties,” it added.

Defining roles, responsibilities

The manual defines the roles and responsibilities of relevant entities by documenting procedures related to public-private partnership contracts, their governance, including proposals from the private sector, market studies, value-for-money assessments, project structuring, and management, in compliance with the 2023 law on regulating federal public-private partnerships.

It also includes instructions on determining priorities for partnership projects between the federal government and private sector, studying and evaluating the proposed project after conducting a comprehensive analysis of it from various aspects, selecting partners, and procedures for submitting bids and offers to potential partners in the private sector.

“By providing this specific framework for organising and implementing partnership projects between the public and private sectors, the manual unifies the mechanisms, standards, and conditions for implementing partnership projects,” the ministry added.

Promoting growth

Mohamed Hadi Al Hussaini, Minister of State for Financial Affairs, highlighted that the UAE is progressing towards empowering and enhancing its path to sustainable economic growth. He said, “In a world where cooperation and integration between the public and private sectors are fundamental pillars for achieving the nation’s aspirations and strengthening its position, this cooperation aims to achieve better value in public spending.”

He added, “The UAE Ministry of Finance is keen on enhancing the partnership between the public and private sectors, recognising their significant role in the social and economic development of the UAE, thereby promoting sustainable economic growth and ensuring comprehensive prosperity for all members of society. Case studies around the world have shown that public-private partnerships enhance efficiency and effectiveness, improve service levels and quality, reduce costs, and optimally utilise resources through innovation, competition enhancement, economic stimulation, and safeguarding individual interests.”

Al Hussaini said, “This manual represents a practical step forward and an open invitation for active participation and positive contribution from the private sector in supporting the UAE’s efforts to develop major strategic projects and support the national economy.”

Priority sectors

In collaboration with strategic partners, the UAE Ministry of Finance has identified priority sectors for the first phase of future partnership projects, including infrastructure, energy, healthcare, social services, and education.

The UAE Ministry of Finance aims to build and manage integrated and effective strategies and enhance cooperation and dialogue between the public and private sectors, given the importance of this collaboration and its impact on various aspects of economic activity. This effort also aims to enhance governance frameworks to maintain government efficiency and flexibility, and develop its relevant tools.

This step contributes to transferring knowledge and experience from the private sector to federal entities, training and qualifying federal employees in managing and operating projects, and implementing projects that provide added value in exchange for public funds.

Source:https://gulfnews.com/business/banking/uae-approves-guidelines-for-public-private-partnerships-1.1719326563207