08 Jun

How to file an application for corporate tax on free zones businesses

Each free zone has its own framework. Based on these frameworks, the income of the free zone persons will not be subject to corporate tax for a specific period

Free Zones are a crucial part of the UAE economy and have a key role to attract foreign investment that plays a pivotal role in the development of the country. Keeping in view the importance of the free zones special rules have been proposed in the corporate tax (CT) public consultation document for the businesses registered in the free zones (hereinafter referred to as ‘free zones persons’).

Each free zone has its own framework. Based on these frameworks, the income of the free zone persons will not be subject to corporate tax for a specific period. According to the consultation document, the CT regime will honor the tax incentives being offered to the free zone persons subject to the condition that free zone persons maintain adequate substance and comply with all regulatory requirements.

To understand the proposed application of CT on the free zone persons, we have considered all possible options and classified the transactions into the following four categories.

Income from businesses in the rest of the world

It has been proposed in the consultation document that the income earned from transactions with businesses located outside of the UAE will be subject to zero per cent corporate tax. The consultation document is silent about the income earned from transactions with individuals located out of the UAE, which we believe will be subject to the same zero per cent corporate tax.

Income from businesses in the same free zone

The consultation document highlights that the income earned from trading with businesses located in the same free zones will be subject to zero per cent corporate tax. The document is silent about the income earned from transactions with individuals located in the same free zones, which we believe will be subject to the same zero per cent corporate tax, but we will have to wait for the law for further clarification regarding this.

If the free zone person is located in the designated zone for value-added tax (VAT) purposes and selling goods to the mainland person on INCO term where delivery of the goods is being given in the designated zone and the mainland party is clearing the goods in its own import code, still designated zone person can benefit from the zero per cent corporate tax.

Income from the persons in other free zones

The consultation document is clear about the proposed application of the corporate tax on the income earned from persons located in other free zones, and these transactions will be subject to zero per cent corporate tax.

Income from persons on the mainland

Free zone persons may have transactions with persons located on the UAE mainland. It is clearly stated in the consultation document that if the mainland entity and free zone person are part of the same CT group, then income earned by the free zone persons will be subject to zero per cent corporate tax. However, to ensure the CT neutrality of such transactions, payments made to the free zone person by a mainland group company will not be an allowable expense to calculate the taxable profits of the group.

If the mainland business and free zone person are not part of the same CT group, then the legal structure of the free zone person is critical. Like, if the free zone person has a branch on the mainland, then the income of the free zone person will be taxed at the regular CT rate on its mainland sourced income, whilst continuing to benefit from the zero per cent CT rate on its other income. However, if the free zone person has no branch on the mainland, then free zone person can continue to benefit from the zero per cent CT rate of its passive income from mainland persons. The passive income would include interest and royalties, dividends and capital gains from owning shares in mainland UAE companies.

Where a free zone person earns income from the mainland persons which is subject to a zero per cent CT rate, such income would be subject to a withholding tax of zero per cent.

Source:https://www.khaleejtimes.com/finance/how-to-file-an-application-for-corporate-tax-on-free-zones-businesses?_refresh=true

06 Jun

UAE readies for GCC’s lowest tax regime as global corporates brace for tariff hikes

The median corporate tax rates in leading economies worldwide fell to a new low of 25.1 per cent in 2021, which is nearly three times of the nine per cent tax rate that the UAE is going to implement from June 2023

Businesses worldwide are bracing for higher tax costs as cash-strapped governments seriously consider increasing taxes on corporates following a period of low tax regime, according to a study by a leading accounting network.

The median corporate tax rates in leading economies worldwide fell to a new low of 25.1 per cent in 2021, which is nearly three times of the nine per cent tax rate that the UAE is going to implement from June 2023.

The study by UHY, the international accounting and consulting network, says that with the Covid-19 pandemic leaving a gaping hole in the public finances of countries around the world, the trend of declining corporate tax rates worldwide is likely to be over for the foreseeable future.

“Countries around the world have wanted to remain competitive by keeping the tax burden on companies as low as possible in recent years. The cash strapped governments of 2022 will likely now be considering increasing taxes on corporations,” said Subarna Banerjee, chairman of UHY.

He said public finances will have to be shored up somehow and corporations can be an easier target politically than individuals. “Businesses worldwide should be prepared for their tax costs to begin to rise in the coming years.” Several countries have announced their intention to raise the tax rate. The UK already announced its intention to raise corporation tax rates to 25 per cent from April 2023, more than two percentage points higher than the European average.

President Joe Biden has also pledged to raise federal corporate income tax to 28 per cent, after it was cut to just 21 per cent by his predecessor Donald Trump in 2017.

Global corporate tax rates have been steadily decreasing over recent years, with the G7 average for a business recording profits of $1.0 million falling from 32 per cent in 2014-15 to just 26 per cent in 2020-21. Many countries sought to incentivise businesses to invest in their economies with attractive tax rates. France, often seen as a higher tax European economy, has lowered its headline rate from 31 per cent to 26.5 per cent in just the past three years.

The UAE, typically renowned as a low-tax jurisdiction, recently introduced corporate tax at one of the lowest rates across the globe — nine per cent — for financial years starting on or after June 1, 2023. “This measure is in line with the UAE’s ambition to establish a more transparent local economy while continuing to retain its attractiveness as a global hub for foreign investment,” the study said.

With the SME and start up sector constituting up to 94 per cent of the UAE economy, the UAE leadership has ensured the economic engine of the business landscape is empowered towards growing strategically while striking a balance in meeting compliance and regulatory obligations that protect businesses in the long haul, said the study.

“In the realm of multinationals, UAE will adhere to the global minimum tax rate of 15 per cent, which 136 countries have agreed to under the aegis of the Organisation for Economic Cooperation and Development (OECD),” it said.

James Mathew, chief executive and managing partner of UHY James Chartered Accountants, said the introduction of corporate tax in the UAE clearly reiterates the nation’s commitment towards aligning its economic environment with global best practices.

“However, the investor friendly corporate tax rate of nine per cent is indicative of the country’s efforts in cementing its position as a destination of choice for foreign investment while building a foundation on tenets of regulatory compliance, legislative obligations, and robust AML (anti-money laundering) measures.”

Mathew said corporate tax will bring a positive ripple effect into play in the UAE economy.

“The arrival of corporate tax in the UAE in 2023 has already put into motion discussions around effective tax planning,” he said.

“SME’s make up 94 per cent of the UAE economy and almost two thirds of the SMEs feel constrained due to lack of access to finance at a reasonable cost. With the introduction of VAT in the UAE in 2018, banks adopted a favourable approach in channelising finance to SMEs and now with corporate tax coming into force, the SME sector will stand to gain significantly with measures that increase the transparency factor of their business,”

Source:https://www.khaleejtimes.com/business/uae-readies-for-gccs-lowest-tax-regime-as-global-corporates-brace-for-tariff-hikes

01 Jun

Application of corporate tax on the individuals and legal persons

If the individual is conducting any commercial activity which requires a licence from the related authorities, the individual would be required to take the permit, and the UAE source income of the individual would be subject to corporate tax

The persons subject to corporate tax (CT), can be classified into natural persons and legal persons. The natural persons who fulfil the criteria would fall under the scope of CT, and in the same way, the legal persons that satisfy the specific conditions would be subject to CT. On the other hand, natural and legal persons who do not meet the criteria would be exempt from CT. In this article, we have covered the proposed treatment of CT on natural persons and legal persons.

Application of CT on the natural person:

The individuals can conduct some activities in the UAE without taking a commercial licence/permit, and such income of individuals would not be subject to CT. For example, individuals’ employment income, dividend income, rental income from the investment in the property and other investment income.

If the investments in the real estate and other areas are held through a private or family trust on behalf of individual beneficiaries, the trust would be subject to the same CT treatment like for a natural person. If the individual family members own the property/properties, they can create trust and shift all their properties under the trust. The trust would be managing all such properties on behalf of the individuals who would be beneficiaries of the income. Such income of the trust will not be subject to CT.

Application of CT on the legal person:

The legal persons can be classified into incorporated persons like limited liability companies (LLC), public joint-stock companies (PJSC), private shareholding companies etc. and unincorporated persons like partnerships, joint ventures (JVs) and associations of persons (AoP). The incorporated persons may be incorporated in the UAE or out of the UAE. If the legal persons are incorporated in the UAE, their worldwide income will be subject to CT, and if the businesses are incorporated out of the UAE, still their income would be subject to CT in the UAE if these businesses:

• are being controlled and managed in the UAE (worldwide income will be subject to CT).

• have Permanent establishment in the UAE (UAE source income will be subject to CT)

• earn any UAE source income (UAE source income will be subject to CT)

Like incorporated persons, unincorporated persons like partnerships, JVs, and AoP may be in the UAE or out of the UAE. If these are in the UAE, businesses would be required to assess whether their partners have limited or unlimited liability. If any of the partners have unlimited liability, these entities are called “transparent” and their income would be subject to CT in the hands of the partners or members. This means that these entities will not be subject to CT but their net taxable income will be subject to CT in the hands of the partners or members. On the other hand, where the liability of all partners is limited, such partnerships will be treated like an incorporated company in the UAE.

If the partners or members are living in the UAE, and unincorporated persons are located out of the UAE, then some countries may treat them as “transparent” entities and others may treat them as a company. Such non-resident unincorporated persons will have the same CT treatment in the UAE like these will have in their respective countries.

The businesses and natural persons are required to assess their status and be prepared for the CT accordingly.

Source:https://www.khaleejtimes.com/finance/application-of-corporate-tax-on-the-individuals-and-legal-persons

25 May

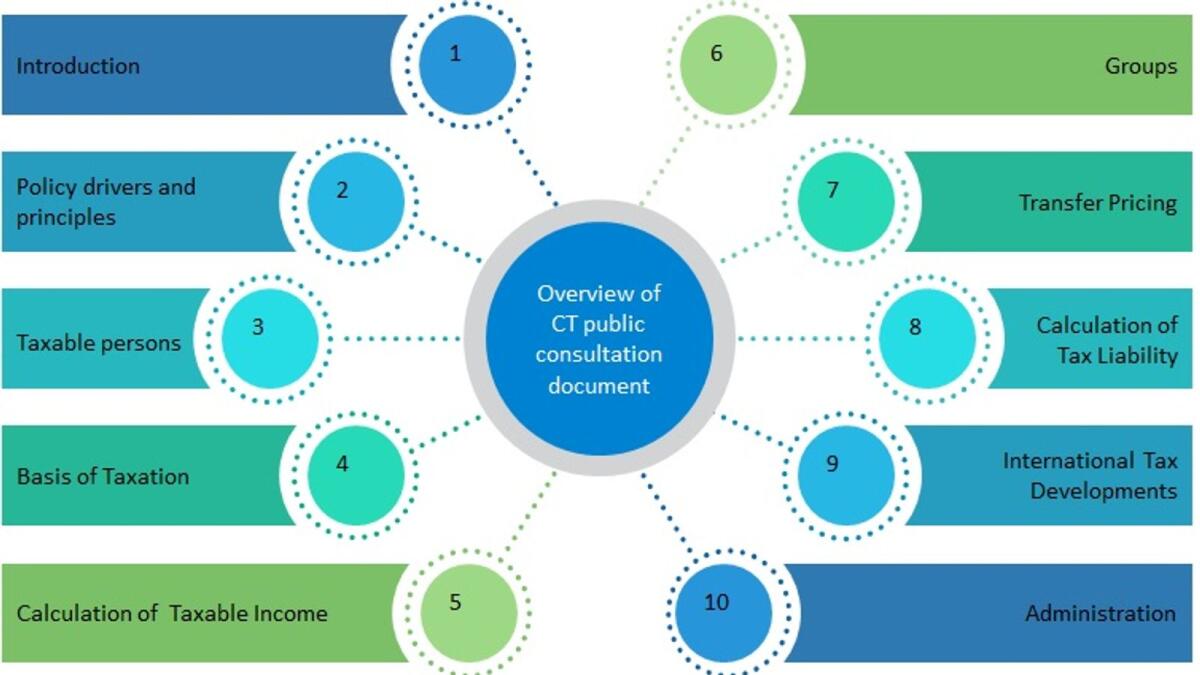

Overview of the corporate tax public consultation document

The consultation document is containing 10 sections starting from the introduction and ending with the administration

On January 31, 2022, the Ministry of Finance (MoF) announced that the UAE will introduce the corporate tax on the taxable profits of the businesses effective from the financial year starting on or after June 01, 2023. In continuation of the finalisation of the UAE corporate tax (CT) regime, on April 28, 2022, the MoF issued the public consultation document to seek the opinion of the stakeholders on the main features and smooth implementation of the corporate tax which would be helpful for the MoF to receive input from the interested parties and make informed decisions.

The consultation document is containing 10 sections starting from the introduction and ending with the administration. In the first and second sections of the consultation document, MoF has highlighted the purpose of issuing the consultation document and the rationale behind the issuance of CT regime in the UAE respectively.

• have Permanent establishment in the UAE (UAE source income will be subject to CT)

• earn any UAE source income (UAE source income will be subject to CT)

The tax on unincorporated partnerships, joint ventures and associations of persons depends upon their presence and liability of their partners.

In the sixth section, it has been given that the UAE resident group of companies can form a tax group and be treated as a single taxable person. Moreover, it covers the conditions to enter into the tax group. The rules related to the transfer of losses, group relief and restructuring relief has been given in detail.

The seventh section highlights that there would be transfer pricing rules and transactions between the related parties would be on an arms-length basis. Arm length principles and documents requirement has been given in this section as well.

In the eighth section, it has been given that the zero per cent tax would be applicable on the taxable income up to Dh375,000, and any taxable income beyond Dh375,000 would be subject to tax at the rate of nine per cent. The zero per cent withholding tax would apply to the following domestic and cross border payments made by the UAE businesses:

• UAE sourced income earned by a foreign company that is not attributable to a PE in the UAE of that foreign company.

• Mainland UAE sourced income earned by a Free Zone Person that benefits from the zero per cent CT regime

• Dividends and other profit distributions made by a Free Zone Person that benefits from the zero per cent

TThe UAE and over 130 other countries reached an agreement on BEPS 2.0. The ninth section will cover the proposed approach by the UAE to respond to BEPS 2.0, and set the basis for the reallocation of profits from where sales arises and the requirement for the global minimum tax of fifteen per cent

A business subject to CT will need to register with the FTA and obtain a tax registration number. Every registered business will be required to file an annual tax return and make payment within nine months from the end of the relevant financial year, and it has been given in the last section of the public consultation document.

Source:https://www.khaleejtimes.com/finance/overview-of-the-corporate-tax-public-consultation-document?_refresh=true